In this article I want to recount the story of a client who came to us for a solicitor’s certificate in respect of a private loan. This is an article that anyone who borrows money privately should read.

Before I get to that, I wanted to thank those who commented on last week’s article about housing affordability. You can access the article by clicking here. It was fascinating to hear from a landlord whose income was declining, a tenant struggling for accommodation and also a more philosophical response.

I also wanted to note that one client will likely save a year’s land tax as a result of reading our article on land tax concessions when moving home. Nice to know that clients get some value from my random musings….

Solicitor’s Certificates

As you may be aware, when a loan is guaranteed by a third party – often a company director or property owner – the lender will require a solicitor’s certificate.

This is essentially a certificate from a solicitor (hence “solicitor’s certificate”) that says, in simple terms that your identity has been formally verified and the loan documents explained to you before you sign them.

We have covered these in more detail in a previous article – click here.

However, our focus today is on a client that decided to walk away from a loan when the details hidden in the loan documents were explained. There were five key reasons for this – which I will explore below.

Accountant’s Certificate

It is relatively common for private lenders to seek assurances from the borrower’s accountant that the borrower’s taxes are paid and the loan is for commercial purposes – as most private lenders aren’t licensed to make consumer loans.

However, there is a trend for private lenders to require further assurances from accountants in an environment where accountants are becoming more reluctant to expose themselves to risks if things go wrong.

In this case the lender wanted the accountant to confirm:

The client was concerned that this was different to what they were told when the letter of offer was issued, the client did not think their accountant would be comfortable issuing this sort of letter.

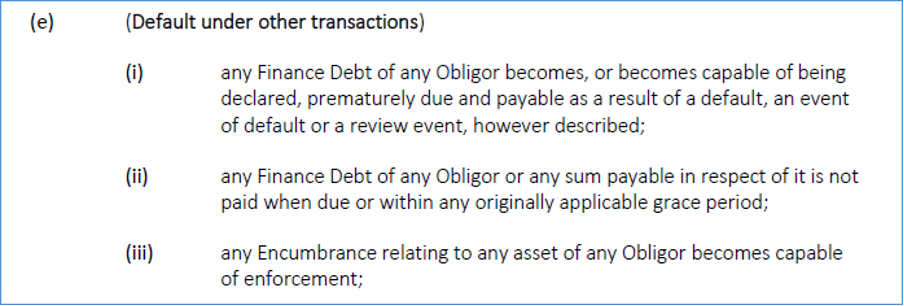

Cross Default

It is common for loan documents to provide that default under another mortgage or secured obligation would constitute a default under this loan agreement.

This particular set of loan documents took this even further:

This default clause does not have a minimum trigger amount or a provision that the default had to endure for more than say 7 days. The client was concerned that a missed credit card payment or an Afterpay facility would constitute an event of default.

Early Repayment Costs and Break Fees

Private lenders often charge interest in advance – which is usually not refundable even if the loan is repaid early.

In this case, the consequences of early repayment and the break costs that would be payable simply weren’t clear. The client was not comfortable with this.

Lender Withdrawal

Most private loan documents provide that the lender can withdraw at any time before the loan settles – without being obliged to provide any reason for withdrawing.

More concerningly, if the Lender does withdraw the loan documents typically provide that the lender will still be entitled to claim the loan application, brokerage and other fees. These fees can amount to substantial amounts of money.

The client in this case was not comfortable with these provisions.

Lender’s Rights

Most loan documents include an extensive list of default provisions, exhaustive rights for lenders on default and a power of attorney in favour of the lender.

The client felt that these rights far exceeded what the lender required to protect their legitimate interests.

Concluding Thoughts

Private loans can be an extremely flexible way to obtain funds when you can’t meet traditional bank lending criteria.

However, you need to be aware of what is likely to be included in private loan documents when you start out down the path of seeking a private loan.

A few key tips:

- Try to use a reputable lender that has a track record;

- Absolutely make sure that you carefully review the letter of offer before you sign it – and understand what fees you will be liable for if you don’t proceed;

- Get legal advice from a lawyer with relevant expertise before you sign the letter of offer and certainly before you sign loan documents.

I have been working in the field of private lending for more than 25 years – as a lender and acting for both lenders and borrowers.

If you are about to sign a letter of offer – please book an appointment with me – at the low fixed fee of $275 (inc GST) before you proceed. You have no further obligation and you will get access to more than 25 years of experience. Click here to book.

Lewis O’Brien

Your Preferred Property Lawyer